News

Buying distressed properties through Bank auctions: JLL

The following is the report by Anuj Puri, Chairman & Country Head, JLL India

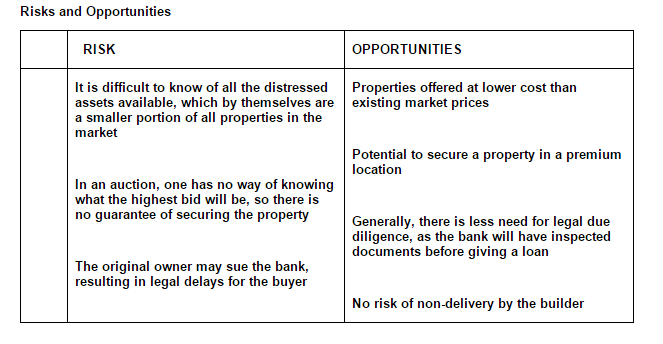

Distressed properties are those where the owner has taken a loan against property to acquire the asset and been unable to service his debt obligations. Due to the owner’s falling behind on the EMI payments for four, five consecutive cycles, the property has been seized by the bank as collateral, and will be sold to recover the interest and unpaid principal amount due to the bank. Such properties are sold through a bank auction and can be acquired at prices which are often well below market value.

Distressed properties are rare, since less than 5 per cent of Indian borrowers default on their obligations for periods long enough to warrant a bank auction. There is also limited scope for getting these properties at throwaway prices, since the base price for the auction is determined by the loan amount outstanding – the further along the owner is in the loan term, the lower the base price. Property owners who have only a few cycles left to repay would prefer to restructure the loan rather than default on payment.

Banks will invariably release an advertisement in all leading local newspapers when they intend to auction off a property or set of properties, so this is the best source of information. A bank’s annual report will always mention a provision for bad debts, and the schedules/annexures would reflect if and when any distressed properties will be coming up for auction.

One may also reach out to a property consultant with expertise in the location and specifically inquire about distressed asset opportunities. The consultant can also represent investors in discussions with the original owner, or directly with the bank.

When a bank places the property for auction, one needs to read the bid document carefully to understand the status of unpaid dues. The bid document is like a prospectus of a IPO, where all the facts covering legal title and responsibility for pending dues are stated. Basis the bid document, one can form an opinion on the status of unpaid dues. Most of the time, the property is sold on a ‘as is where is’ basis and till the date of auction, dues are cleared.

Bank Auction: Of both possible processes, this is lengthier one, with the bank releasing an advertisement, setting a date for the auction, inviting bids, collating the offers and then finally deciding who to sell the property to. It can be even more cumbersome if the buyer himself wants a loan to purchase the property either through the same bank or a different bank. The process also takes longer because the bank has to conduct a thorough due diligence search on the incoming buyer and then draw up contracts to transfer the property along with a go-ahead from the owner, and a society NOC.

The bank will obtain an NOC from the society or condominium before conducting the auction. Many societies and their members have first right of refusal, or its members can match the highest bid to buy the property. At the time of obtaining NOC, the society will highlight any liabilities that the new owner will have to bear, and if if any neighbour has been impacted. The banks and its legal counsels will capture such aspects in the bid document, and the bidder can refer to them to assess the liability.

Directly from the actual owner: In this case, the owner and the new buyer would agree on the commercial terms, exchange a token deposit and then complete the bank process to continue with purchase before signing the agreement and accordingly taking possession. The entire bank process of releasing the property, granting the NOC and acquiring the society NOC, as well as repaying the bank loan, can take as long as 2–3 months. The price available here is generally higher than it would be in a bank auction, since the seller will try to recover as much of his initial investment as possible.

Precautions buyers must exercise to avoid risks: Buyers must read the bid document carefully to understand the status of unpaid dues or other liabilities, and should be fully aware of what they are getting in to while buying a distressed property, and aim for a win–win for the bank and the original owner so that there is a limited scope for a legal challenge. They must focus on understanding the history of the property under discussion and also get any historical papers for title due diligence.

Omaxe Chowk Launches “Filmy” Campaign: Highlights Modern Shopping Experiences in Medieval Chandni Chowk

Delhi, April 24, 2024: Omaxe Chowk, the commercial destination in the heart of Chandni Chowk, Old Delhi, released a ‘film dialogue-based’...

SKA Forays In Luxury Housing: Launches SKA Destiny One in Greater Noida, To Invest Rs 592 Crores

New Delhi, April 24, 2024: NCR based real estate developer, SKA Group announced its foray into the luxury segment and...

Unlocking Investment Potential: Exploring Yamunanagar’s Real Estate Landscape

By: Ravi Saund, Founding Director, Emperium Nestled in the heart of Haryana, Yamunanagar is not just any ordinary city; it’s...

‘Great Indian Comic Book Festival’ from Apr 26-28, 2024 at Pacific Tagore Garden

New Delhi, April 24, 2024: Pacific Tagore Garden is organizing the ‘Great Indian Comic Book Festival’, scheduled from April 26...

NCR Saw 29 Land Deals for Nearly 314 Acres Closed in FY-24: ANAROCK Report

New Delhi, April 24, 2024: Delhi-NCR continues to be a hotspot for real estate transactions across various sectors and as in the...

hBits Forays in Pune, Acquires Grade A Commercial Property in Magarpatta

Pune, April 24, 2024: hBits, a leading fractional ownership platform, has marked its entry in Pune with the acquisition of...

-

News3 weeks ago

News3 weeks agoKW Delhi 6 Mall Onboards New Brands

-

News4 weeks ago

Manasum Senior Living Launches IKIGAI GOA, A Senior Living Community in North Goa, in collaboration with Prescon Homes

-

News2 weeks ago

Godrej Properties Sells Rs 3k cr+ Homes of Godrej Zenith, Gurugram, within 3 days

-

News4 weeks ago

Bridging India Divide: Top 5 Tier- 2 Cities to Focus On

-

News3 weeks ago

Commercial Realty Gets Tech Savvy: Fast Construction, Enhanced Convenience

-

News4 weeks ago

Multipoint Connection – A Definite Boon

-

News3 weeks ago

RBI’s Status Quo on Key Policy Rates to Help Maintain the Real Estate Growth Momentum, Say Industry Stalwarts

-

News1 week ago

Olive Announces Dhruv Kalro as Co-Founder