News

CBRE’S GST Survey: Almost 70% Of Occupiers Optimistic About The Impact Of GST On Supply chain/ Warehousing Business

80% of respondents felt that the taxation system improved after the implementation of GST

- 40% of respondents indicated that they would increase the number of warehouses in the post-GST era

- More than 60% of the respondents indicated that they prioritize better partnerships or JVs with global service providers in the post-GST era; resulted in more than USD 500 million of investment into the I&L sector between 2017 and H1 2019

- Infusion of technology and innovative business strategies are catalyzing growth in the sector

New Delhi, 15th, October 2019: CBRE South Asia Pvt. Ltd, India’s leading real estate consulting firm, today announced the findings of its latest survey titled “Towards a Unified India 2.0: How did Warehousing Occupiers approach the GST?”. The results of this year’s survey highlight how well occupiers have adjusted to the new tax regime and what is really driving the sudden growth of the Industrial and Logistics sector (I&L) in India.

Anshuman Magazine, Chairman & CEO – India, Southeast Asia, Middle East & Africa, CBRE said, “The logistics sector in India is headed towards transformative growth. The permeation of technology in operations, innovative business models & strategies, improving supply chain efficiencies, augmented warehousing demands, varied funding avenues, favorable government policies, geographical expansions into tier II and III cities are together playing an instrumental role in preparing the sector for the next phase of development. Given the fundamental shifts across the I&L sector in just two years, coupled with increasing demand for quality space, developers are more likely to build compliant, large-sized spaces. We estimate that the rising interest of prominent players is likely to result in the country’s warehousing stock touch 500 million sq. ft. by 2030.”

This is the second report in this series, the first report having been released immediately after the implementation of the GST in 2017. The timeline of the findings of our first survey has been referred to as the pre-GST era throughout this report, while that for our recent survey has been referred to as the post-GST era.

Jasmine Singh, Nation Head– Industrial & Logistics Services & Senior Executive Director Advisory & Transactions Services, CBRE India, said, “This survey seeks to assist investors, asset managers, and developers in gaining a deeper understanding of the occupiers’ current and future requirements in the post-GST era. It aims to aid occupiers to gauge key trends in the market and make better decisions. It will also help the entire I&L industry to map how all stakeholders are responding to the GST.”

“Towards a Unified India 2.0: How did Warehousing Occupiers approach the GST?”, the second report looks closely at the impact of the new tax regime across the entire lifecycle of a warehouse. Enclosed below are some excerpts of how the new taxation regime has affected the I&L sector at every step:

Planning:

- Occupiers’ intent to expand operations was quite visible as 40% of our respondents indicated that they would increase the number of warehouses in the post-GST era.

- Occupiers continue to consolidate and expand operations, driven by the growing need to develop mother hubs close to demand centers.

- The respondents highlighted the quality of space (about 90%) and large-sized, efficient warehouses (about 75%) as the most important factors while selecting the location of a facility.

Building:

- The advent of global players and increasing demand for quality spaces has boosted the demand for purpose-built spaces.

- The intent to directly lease space in a warehouse has also increased in the post-GST era. This has been on account of two factors – 1) the need to be “in the market” quickly and 2) the ready availability of such spaces.

Transacting:

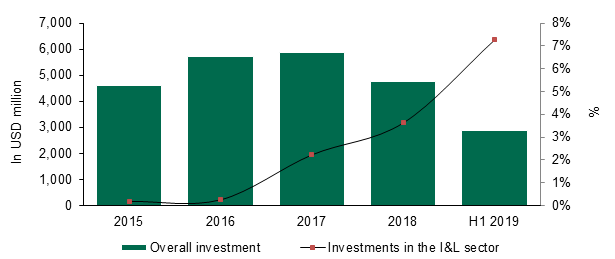

- Several policies (both proposed and implemented), along with the grant of ‘infrastructure status’ to the logistics sector, led to more than USD 500 million being invested in acquiring I&L assets in India during 2017- H1 2019.

-

Transacting:

- Several policies (both proposed and implemented), along with the grant of ‘infrastructure status’ to the logistics sector, led to more than USD 500 million being invested in acquiring I&L assets in India during 2017- H1 2019.

- Several policies (both proposed and implemented), along with the grant of ‘infrastructure status’ to the logistics sector, led to more than USD 500 million being invested in acquiring I&L assets in India during 2017- H1 2019.

Managing / Operations & Maintenance:

- Respondents were positive about the impact of GST across the entire supply chain – about 70% said they would optimize their sourcing models while more than half reported an improvement in working capital management techniques.

- Occupiers (more than 60% of the respondents) felt that the overall operating costs within a warehouse were bound to rise due to the deployment of tech and increasing adherence to global compliance norms in the post-GST era.

Traditionally, the regulatory environment with multiple taxes across the states played a primary role in the performance and potential growth of the I&L sector in India. However, with the implementation of the GST and several other policies, the regulatory environment has significantly changed.

- Almost 70% indicated an improvement in ease of doing business, citing the example of e-way billing in this regard. E-way billing, in particular, has removed a majority of bottlenecks in cargo storage and transport processes

- Moreover, digitization of the regulatory set-up in the post-GST era has further resulted in a more convenient, user-friendly interface for filing indirect tax returns

What’s next for the I&L sector in India: The Eleven Commandments

Over the past two years, both occupiers and developers have been able to realign business strategies to optimize costs and supply chain efficiencies. Given the radical shifts across the I&L sector in just two years, this CBRE report expects that the following trends would occur going forward:

- Warehousing demand will strengthen: I&L absorption is anticipated to be about 10-15% higher than in 2018 – about 25-30 million sq. ft. would be leased in 2019

- The rising activity of global/organised players: The rising interest of prominent players is likely to result in the country’s warehousing stock touch 500 million sq. ft. by 2030

- Moving towards integrated logistics parks: Given the rising activity of prominent developers in the I&L sector, coupled with the increasing requirements of occupiers, we expect that the size of warehouses would continue to increase over the next few years

- Evolving alternative segments within the I&L sector: The I&L sector is expected to soon see stakeholders concentrate on meeting niche requirements – which cater to specific needs such as cold storage and green logistics solutions. The cold storage segment is expected to witness an increase in demand from F&B occupiers such as Zomato, which is already in the business of supplying fresh raw material to restaurants. This is expected to eventually give rise to the concept of ‘dark kitchens’[1].

- Varied funding avenues: With strong demand-supply dynamics, the I&L sector is likely to offer investors an increasing number of options to enter the country. The launch of India’s first REIT has also paved the way for I&L developers to accumulate REIT-compliant portfolios and include them in further launches in India

- The rapid adoption of tech: Tech would continue to pervade all stages of the lifecycle of a warehouse, thereby improving the quality of upcoming supply.

- Improved regulatory environment: For the first time, dedicated policies including Draft e-Commerce Policy, Draft Logistics Policy, Data Protection Policy and Draft Industrial Policy are likely to be formalized in the coming quarters.

- Improved infrastructure connectivity: Various infrastructure initiatives including Bharatmala, Sagarmala, Inland Waterway Act, Trade Infrastructure for Export Sector (TIES), Logistics Efficiency Enhancement Program (LEEP) and Vehicle Fleet Motorization Program (VMP) would further boost supply chain efficiencies across the country.

- Penetration into tier II and III cities: The share of tier-II cities in logistics shipments in India is expected to grow from almost 40% in 2017 to about 50% in 2022[2], thereby directly competing with tier I / metro cities. Additionally, with the aforementioned demand drivers including the advent of e-commerce companies and the integration of warehouses with brick-and-mortar retailing, we expect that occupiers would now consider operating in tier II & III cities – about 60% of our respondents agreed with this assessment

- Shared warehousing: As the culture of the sharing economy spills over across RE segments, we believe that shared warehousing is likely to gain strength in the coming years. The trend is expected to be more pronounced in core markets, where rentals are high, reach to market is important and supply is a concern.

- Demand for ‘last-mile’ warehouses likely to grow: As large distribution centres proliferate, the demand for ‘last-mile’ warehouses are expected to increase, with same-day delivery expected to become the new standard for the I&L sector. According to CBRE Research, such warehouses must be located within the limits of a densely populated city to ensure the delivery of goods within a few hours.

Omaxe Chowk Launches “Filmy” Campaign: Highlights Modern Shopping Experiences in Medieval Chandni Chowk

Delhi, April 24, 2024: Omaxe Chowk, the commercial destination in the heart of Chandni Chowk, Old Delhi, released a ‘film dialogue-based’...

SKA Forays In Luxury Housing: Launches SKA Destiny One in Greater Noida, To Invest Rs 592 Crores

New Delhi, April 24, 2024: NCR based real estate developer, SKA Group announced its foray into the luxury segment and...

Unlocking Investment Potential: Exploring Yamunanagar’s Real Estate Landscape

By: Ravi Saund, Founding Director, Emperium Nestled in the heart of Haryana, Yamunanagar is not just any ordinary city; it’s...

‘Great Indian Comic Book Festival’ from Apr 26-28, 2024 at Pacific Tagore Garden

New Delhi, April 24, 2024: Pacific Tagore Garden is organizing the ‘Great Indian Comic Book Festival’, scheduled from April 26...

NCR Saw 29 Land Deals for Nearly 314 Acres Closed in FY-24: ANAROCK Report

New Delhi, April 24, 2024: Delhi-NCR continues to be a hotspot for real estate transactions across various sectors and as in the...

hBits Forays in Pune, Acquires Grade A Commercial Property in Magarpatta

Pune, April 24, 2024: hBits, a leading fractional ownership platform, has marked its entry in Pune with the acquisition of...

-

News3 weeks ago

KW Delhi 6 Mall Onboards New Brands

-

News4 weeks ago

Manasum Senior Living Launches IKIGAI GOA, A Senior Living Community in North Goa, in collaboration with Prescon Homes

-

News2 weeks ago

Godrej Properties Sells Rs 3k cr+ Homes of Godrej Zenith, Gurugram, within 3 days

-

News4 weeks ago

Bridging India Divide: Top 5 Tier- 2 Cities to Focus On

-

News3 weeks ago

Commercial Realty Gets Tech Savvy: Fast Construction, Enhanced Convenience

-

News4 weeks ago

Multipoint Connection – A Definite Boon

-

News3 weeks ago

RBI’s Status Quo on Key Policy Rates to Help Maintain the Real Estate Growth Momentum, Say Industry Stalwarts

-

News1 week ago

Olive Announces Dhruv Kalro as Co-Founder