News

India to require 1.3 billion sq ft additional healthcare space by 2030: CBRE Report

June 2, 2022: CBRE South Asia on Thursday published its first-ever report on India’s healthcare sector – ‘The Evolving Indian Healthcare Ecosystem: What It Means for the Real Estate Sector’. The report highlights the trends expected to redefine the healthcare landscape and delivery in the country in the coming times.

The report also states that India has one of the lowest bed-to-population ratios in the world, which is indicative of the infrastructure gap as well as the vast growth potential of this segment. The report ran an analysis to identify this growth potential to understand how much real estate space hospitals would require to ensure equitable distribution of health services in the country by 2030. As per the report, India will require an additional 1.3 billion sq. ft. of healthcare space to improve the infrastructure disparity.

The growing incidence of cancer and cardiovascular diseases, and the COVID-19 pandemic have helped identify the challenges that exist in terms of infrastructure and flexibility to cater to sudden influx of patients and capacity building. Most of these challenges existed prior to the pandemic, but have come now come to greater focus. However, the growing levels of awareness towards these challenges and the will to address them have led to an improved policy and spending scenario on the government’s part and widening private sector participation.

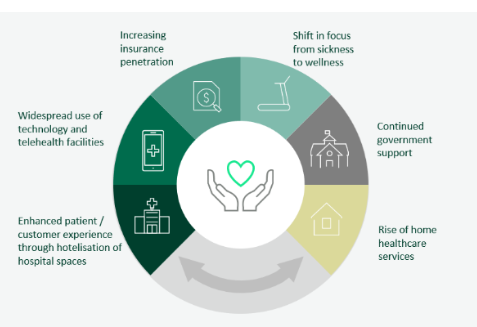

The report further highlighted the key trends in the healthcare space that are driving its transformation and what industry stakeholders can do to drive positive outcomes:

Trend Way forward Accelerating demand for quality healthcare in tier II and III cities. Tier II and III cities such as Nashik, Indore, Visakhapatnam, Jaipur, Mohali, Surat and Dehradun are already witnessing a growing presence of healthcare providers. Players operating in this space can also consider cities such as Ludhiana, Guwahati, Rajkot and Mysore amongst others which have a high population and relatively higher spending propensity on facilities such as healthcare. Decline in the number of elective and outpatient (OPD) cases, leading to a loss of revenue. This trend is already reversing with a significant resurgence in the number of surgeries as the pandemic abates. However, the uncertainty calls for better operational efficiency by identifying compressible cost heads such as manpower, supply chain etc. Hospitals can also consider strategies such as providing quality home care, especially for surgical recoveries, and investing in telehealth, which can significantly widen the revenue base. Requirement of holistic healthcare models that ensure better health outcomes and consumer satisfaction.+Limited availability of healthcare professionals due to steep rise in workload, increase in risk of infections. Hospitals can focus on developing a universal health interface. It can consist of home care, wellness clinics as well as outreach clinics in high traffic areas that can supplement the hospital as the nodal healthcare provider. Hotelisation of spaces by making the facilities less “hospital-like” and addition of amenity spaces (such as shopping arcades and eateries) would help enhance patient experience. Investment in development of facilities specially developed for post-surgery or recovery care would help reduce workload as well as increase patient comfort and confidence in visiting such establishments.

Anshuman Magazine, Chairman & CEO – India, South-East Asia, Middle East & Africa, CBRE shared, “Healthcare in India is being driven by rising income levels, growing health awareness, better access to medical insurance amidst increasing government spending on healthcare, an ageing population and the changing nature of epidemiology. COVID-19 underlined the importance of this segment, thereby amplifying investor interest. Moreover, the pandemic has ensured that in addition to health facilities, other functions too have entered the mainstream to forge a new ecosystem. These include telehealth / healthtech, deeper penetration of medical insurance, rise of quality home healthcare services, focus on patient experience and hospital environment, and transition from disease cure to prevention and wellness.”

Implications for different real estate segments:

- Land (hospital chains, clinics): As mentioned previously, the hospital segment is expected to require an additional 1.3 billion sq. ft. of space to match global bed-to-population standards. We, therefore, expect further expansion by hospital players, leading to a spurt in demand for land across the country. Moreover, as the hospital-and-clinic model gains precedence, peripheral areas of tier I cities as well as high traffic areas in tier II and III locations would see land acquisition for setting up clinics.

- Industrial and logistics real estate: Due to specific storage needs of life-saving pharmaceuticals and vaccines, the demand for warehouse spaces will grow manifold. As access to healthcare increases, this demand could spread to Tier II and III regions. Owing to the rising demand for medical products and pandemic-related difficulties including mobility restrictions and infection spikes in certain areas, reshoring of medical supply chains is also likely.

- Wellness-driven med-tail evolution: The rising emphasis on experience and customer happiness is driving healthcare and wellness companies to retail settings including shopping malls and big box retail formats. The concept of ‘med-tail’ is gaining traction in the West, and its echoes can be heard in India, where wellness facilities are popping up in retail areas. We expect this trend to widen in the future to include aesthetic dermatology, dental treatment, and other services.

- Impact on office and residential sectors: The emphasis on experience may result in a reconfiguration of hospital spaces, which could result in corporate operations such as administration being moved away from the main campus. This would generate demand for office space to accommodate these functions. Meanwhile, increased emphasis on health and wellness would lead residential developers to include a healthcare component in their future projects. For this, developers could either open their own healthcare centres or partner with third-party providers.

How does real estate design and strategy change?

- More focus on air quality, filtration and ventilation; separate air-handling for rooms

- Flexibility in building design; unidirectional corridors, single rooms, isolation rooms, negative pressure rooms to minimize infection risk

- Use of anti-bacterial and non-porous building material; easy-to-clean and -sanitize furniture

- Greater use of technology; touchless designs, automatic doors, video conferencing in OPDs, rooms and OTs

- Outpatient centres / clinics** likely to emerge as a key growth strategy to provide more comfort and access to patients

Investment and business landscape in healthcare:

The Indian healthcare space has witnessed large-scale primary capital infusion in the past, with several of the key hospital, pharmacy and diagnostics chains such as Fortis Healthcare, Apollo Hospitals and Dr Lal Pathlabs being listed on the Indian bourses. Rainbow Hospitals, a single specialty player, was the latest on this list, having issued its IPO early in May 2022. However, the past two years have seen limited primary capital infusion in the overall healthcare space, including the hospital segment. Most of this infusion was witnessed in the healthtech segment, with the emergence of unicorns such as PharmEasy, Curefit and Pristyn Care.

However, capex investments that were done by hospitals a couple of years ago are up for maturity and the need for fresh capital is anticipated. Key hospital and pharmacy (especially e-pharmacy) players are likely to require fresh capital, due to which we expect heightened PE and IPO activity in this space in the coming year.

Provident Housing Secures Rs 1,150 Crores Investment from HDFC Capital, with a Potential GDV of Rs 17,100 Crores

Delhi, April 25, 2024: Provident Housing Limited, a wholly owned subsidiary of Puravankara Limited, announced a Rs 1,150 crore investment...

Lohia Global Forays into Real Estate, Earmarks Rs 1000 Crore Investment

New Delhi, April 25, 2024: Lohia Global has announced its venture into the Indian real estate market with Lohia Worldspace. Led by Pyush...

Sumadhura Group Acquires 40 Acres of Residential Land Parcel in Bengaluru

Bengaluru, April 25, 2024: In the midst of a significant upswing in the real estate market in Bengaluru, Sumadhura Group on...

Omaxe Chowk Launches “Filmy” Campaign: Highlights Modern Shopping Experiences in Medieval Chandni Chowk

Delhi, April 24, 2024: Omaxe Chowk, the commercial destination in the heart of Chandni Chowk, Old Delhi, released a ‘film dialogue-based’...

SKA Forays In Luxury Housing: Launches SKA Destiny One in Greater Noida, To Invest Rs 592 Crores

New Delhi, April 24, 2024: NCR based real estate developer, SKA Group announced its foray into the luxury segment and...

Unlocking Investment Potential: Exploring Yamunanagar’s Real Estate Landscape

By: Ravi Saund, Founding Director, Emperium Nestled in the heart of Haryana, Yamunanagar is not just any ordinary city; it’s...

-

News4 weeks ago

News4 weeks agoKW Delhi 6 Mall Onboards New Brands

-

News4 weeks ago

Manasum Senior Living Launches IKIGAI GOA, A Senior Living Community in North Goa, in collaboration with Prescon Homes

-

News4 weeks ago

Bridging India Divide: Top 5 Tier- 2 Cities to Focus On

-

News4 weeks ago

Commercial Realty Gets Tech Savvy: Fast Construction, Enhanced Convenience

-

News3 weeks ago

Godrej Properties Sells Rs 3k cr+ Homes of Godrej Zenith, Gurugram, within 3 days

-

News4 weeks ago

Multipoint Connection – A Definite Boon

-

News3 weeks ago

RBI’s Status Quo on Key Policy Rates to Help Maintain the Real Estate Growth Momentum, Say Industry Stalwarts

-

News1 week ago

Olive Announces Dhruv Kalro as Co-Founder