News

Industrial & Warehousing absorbs 44 million sq ft space in 2021: Savills India

January 6, 2022: Industrial and warehousing space absorption stood at 44 mn sq. ft in 2021 to include 35.1 mn sq. ft from Tier I cities and 8.6 mn sq. ft from Tier II & III cities. Inspite of Covid restrictions and lockdowns impacting construction activities, India witnessed a fresh supply of 45 mn sq. ft. in 2021 where 36 mn sq. ft was from Tier I cities and 8.9 mn sq. ft from Tier II & III cities, as per data released by International real estate advisory firm Savills India.

Supply & Absorption in Tier I (2021 vs 2020)

2021 2020 Y-o-Y change Supply (Mn sq. ft) 36 22 63.6% Absorption (Mn sq. ft) 35.1 26 35% Stock (Mn sq. ft) 266 230 15.6%

* includes absorption & supply in completed Built-to-Suit (BTS) projects

Supply & Absorption in Tier I in 2021

City Supply (million sq. ft) Absorption (million sq. ft) Bangalore 3.5 4.6 Chennai 2.7 3.5 Pune 4.4 6.5 Mumbai 7.5 6.0 Delhi-NCR 11.4 8.1 Hyderabad 2.0 1.6 Kolkata 3.4 3.4 Ahmedabad 1.1 1.3 Total (Tier I) 36.0 35.1

* includes absorption of newly completed Built-to-Suit (BTS) projects

Supply & Absorption in Tier II & III Cities in 2021

City Supply (million sq. ft) Absorption (million sq. ft) Coimbatore 1.29 1.34 Guwahati 0.71 0.67 Indore 0.45 0.93 Nagpur 1.53 1.15 Lucknow 1.09 1.09 Jaipur 0.52 0.42 Rajpura 1.27 1.18 Bhubaneswar 0.03 0.05 Kochi/Ernakulam 0.28 – Patna 0.39 0.49 Hosur 1.29 1.29 Total (Tier II & III) 8.9 8.6

* includes absorption of newly completed Built-to-Suit (BTS) projects

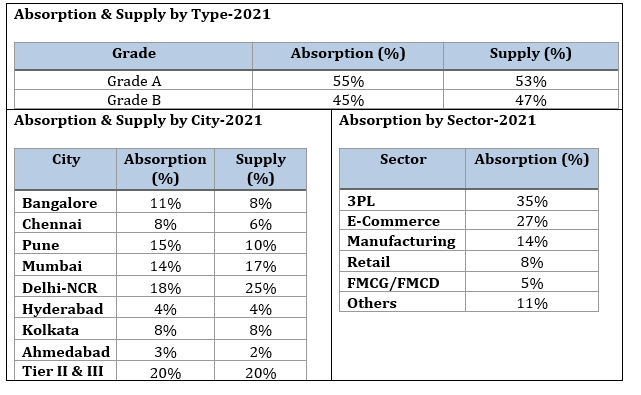

Similar to 2020, 3PL and e-commerce sectors continued to drive warehousing demand accounting 62% of the total absorption in 2021, followed by manufacturing sector at 14%.

Among the major cities in India, Delhi NCR led with the highest absorption in 2021 at 18% followed by Pune at 15%. Mumbai and Bangalore saw absorptions at 14% and 11% respectively, while tier II & tier III cities accounted for 20%.

In addition,the Tier II & Tier III cities such as Rajpura, Lucknow, Coimbatore, Jaipur, Guwahati, Bhubaneswar, Nagpur, Kochi/Ernakulam, Indore, Hosur, and Patna witnessed around 8.6 mn sq. ft of absorption in 2021. These cities are poised to gain further momentum in 2022 and 2023 with e-commerce and 3PL firm capitalizing on consumption-driven growth and pushing the demand for warehousing space.

The overall industrial and warehousing space stock in Tier I cities is at 266 mn sq. ft at end of 2021 and is expected to reach 304 mn sq. ft. in 2022 and 345 mn sq. ft. in 2023. Meanwhile, Vacancy levels in Tier I cities have increased from 8.4% in 2020 to 9.4% in 2021 and rental values remained stable in 2021 across the major cities with new projects delivered with improved specifications and of high quality environmental, health & safety (EHS) standards.

The market witnessed 4,200 plus acres of manufacturing and warehousing land transactions across Tier I and Tier II cities of which 51% was private land and 49% was government land.

The report further highlights that the industrial and logistics sector witnessed investments exceeding USD 1.5 billion in 2021 making the sector the highest after the office sector to attract such investments. Continued interest in this asset class was due to its growth potential and stable returns. The market is likely to witness continued and growing interest from investors in this asset class in 2022 as well.

“Work From Home and social distancing norms have further fuelled the e-commerce demand and therefore growth of the Indian logistics and warehousing sector. Rising popularity of quick commerce companies and e-commerce companies focusing on improving the delivery time and customer experience will result into rapid growth of Urban warehousing. Besides, strong macro-economic fundamentals, government initiatives favouring infrastructure development in transport, water, power and communications and support to the growing sectors are likely to drive manufacturing and warehousing demand in India in 2022”. Srinivas N, Managing Director, Industrial and Logistics, Savills India.

According to Savills India, growing demand for warehouse space for manufacturing, e-commerce and organised retail are likely to drive warehousing demand in 2022. Besides, Warehousing policy envisaged by NHAI would be out in 2022, which aims to develop warehousing zones on the National Highways Authority of India (NHAI) land banks under Public Private Partnership (PPP) mode, proposed national logistics policy by department of commerce likely to ease the logistics bottlenecks and development of Multi-Model Logistics Parks (MMLPs) will certainly push the growth of warehousing in the country. The market is likely to see absorption in excess of 40 mn sq.ft (including Tier I, II & III cities) in 2022. On the supply side, Savills India expects around 45+ mn sq. ft during the same period.

Industrial and logistics properties, especially warehouses, have been at the top of the investors’ list for a while now. The sector will continue to tap into megatrends such as the growth of e-Commerce and every market in the region is undersupplied with modern logistics space. Existing growth potential, the government’s clear strategy and India’s cost advantage are helping to attract sizeable foreign investment into the manufacturing, logistics and warehousing sectors.

Omaxe Chowk Launches “Filmy” Campaign: Highlights Modern Shopping Experiences in Medieval Chandni Chowk

Delhi, April 24, 2024: Omaxe Chowk, the commercial destination in the heart of Chandni Chowk, Old Delhi, released a ‘film dialogue-based’...

SKA Forays In Luxury Housing: Launches SKA Destiny One in Greater Noida, To Invest Rs 592 Crores

New Delhi, April 24, 2024: NCR based real estate developer, SKA Group announced its foray into the luxury segment and...

Unlocking Investment Potential: Exploring Yamunanagar’s Real Estate Landscape

By: Ravi Saund, Founding Director, Emperium Nestled in the heart of Haryana, Yamunanagar is not just any ordinary city; it’s...

‘Great Indian Comic Book Festival’ from Apr 26-28, 2024 at Pacific Tagore Garden

New Delhi, April 24, 2024: Pacific Tagore Garden is organizing the ‘Great Indian Comic Book Festival’, scheduled from April 26...

NCR Saw 29 Land Deals for Nearly 314 Acres Closed in FY-24: ANAROCK Report

New Delhi, April 24, 2024: Delhi-NCR continues to be a hotspot for real estate transactions across various sectors and as in the...

hBits Forays in Pune, Acquires Grade A Commercial Property in Magarpatta

Pune, April 24, 2024: hBits, a leading fractional ownership platform, has marked its entry in Pune with the acquisition of...

-

News3 weeks ago

News3 weeks agoKW Delhi 6 Mall Onboards New Brands

-

News4 weeks ago

Manasum Senior Living Launches IKIGAI GOA, A Senior Living Community in North Goa, in collaboration with Prescon Homes

-

News2 weeks ago

Godrej Properties Sells Rs 3k cr+ Homes of Godrej Zenith, Gurugram, within 3 days

-

News4 weeks ago

Bridging India Divide: Top 5 Tier- 2 Cities to Focus On

-

News3 weeks ago

Commercial Realty Gets Tech Savvy: Fast Construction, Enhanced Convenience

-

News4 weeks ago

Multipoint Connection – A Definite Boon

-

News3 weeks ago

RBI’s Status Quo on Key Policy Rates to Help Maintain the Real Estate Growth Momentum, Say Industry Stalwarts

-

News1 week ago

Olive Announces Dhruv Kalro as Co-Founder