Guest Column

Post DeMo and RERA, Branded Developers Dominate with 53% of New Housing Supply in H1 2019

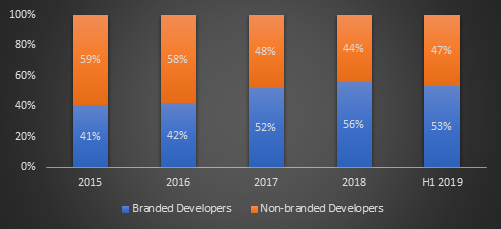

- Top 7 cities saw 73,930 units launched by branded players; 65,550 units by non-branded players in H1 2019

- Prior to DeMo & RERA in H1 2016, non-branded developers dominated by 60:40

- Since H1 2017, share of new launches by branded players saw steady rise; fly-by-night operators exited, smaller players consolidating with big brands

An integral parts of Indian residential real estate’s coming-of-age process is the rise of *branded developers, who are outpacing their non-branded competition in overall housing launches. Reformatory changes led by demonetization and RERA have spearheaded this movement.

ANAROCK research indicates that out of the total new supply in H1 2019 – approx. 1,39,480 units in the top 7 cities – over 53% (73,930 units) were launched by branded developers, and 47% by non-branded entities. In H1 2018, branded developers’ share was 52% and during H1 2016 – before DeMo and RERA – non-branded developers had a 60% share (approx. 95,600 units) of the total of 1,59,090 newly-launched units in the top 7 cities. Branded developers accounted for 63,490 units (40%) of the total supply in the period.

*Branded developers include listed developers, players actively operating for 10 years or more, newly-formed entities of large conglomerates, and players with sizeable areas under development either locally or pan-India.

The Shifting Post-Reforms Power Balance

The aftermath of DeMo was first felt in H2 2016 itself. In H1 2016, the ratio between the supply of branded vs non-branded changed from 40:60 to 46:54 in the H2 2016 – the DeMO period. Thereafter, the change has been significant with supply from branded players overtaking that of non-branded ones.

For instance, in H1 2018, as many as 87,580 units were launched across the top 7 cities. Out of this total, nearly 52% (comprising approx. 45,540 units) were launched by branded developers while the remaining 48% (42,040 units) were by the non-branded players. With the share of branded players increasing to 53% in H1 2019, the writing is clearly on the wall.

Branded vs Non-Branded Supply: Y-o-Y Change

Source: ANAROCK Research

The Change Catalysts

This tectonic shift in the Indian residential real estate sector is the natural outcome of two major and very perceptible change catalysts, and one subtle but profound realignment in the overall demand profile:

Multiple policy reforms left little room for growth to smaller developers and absolutely none for outright fly-by-night players, who are exiting the market rapidly.

The severe liquidity crisis that has beset the real estate sector compels smaller developers to either perish or join hands with their branded, better-capitalized counterparts – effectively reducing their numbers. As long as the liquidity crunch prevails, the gap between the branded and non-branded players will widen in favour of the former.

Millennials’ preference for branded products is no longer limited to electronic goods, fashion and furniture – it now extends to their choice of homes, as well. Branded homes are perceived to be superior in terms of lifestyle quotient as well as investment value appreciation. Increasingly, millennials will compromise on property size in favour of a well-known developer brand which ensures high-grade locations, construction quality and project amenities.

All Buyers Benefit

Not for the first time, the millennial generation has kick-started a progressive trend which benefits the who consumer value chain. Leading developer brands which earlier restricted their efforts to niche luxury offerings are now venturing into the high-demand affordable and mid-segment categories. Their increased supply gives buyers at large the option of investing in homes by the top names in the real estate industry, and thereby availing of all the associated benefits.

Omaxe Chowk Launches “Filmy” Campaign: Highlights Modern Shopping Experiences in Medieval Chandni Chowk

Delhi, April 24, 2024: Omaxe Chowk, the commercial destination in the heart of Chandni Chowk, Old Delhi, released a ‘film dialogue-based’...

SKA Forays In Luxury Housing: Launches SKA Destiny One in Greater Noida, To Invest Rs 592 Crores

New Delhi, April 24, 2024: NCR based real estate developer, SKA Group announced its foray into the luxury segment and...

Unlocking Investment Potential: Exploring Yamunanagar’s Real Estate Landscape

By: Ravi Saund, Founding Director, Emperium Nestled in the heart of Haryana, Yamunanagar is not just any ordinary city; it’s...

‘Great Indian Comic Book Festival’ from Apr 26-28, 2024 at Pacific Tagore Garden

New Delhi, April 24, 2024: Pacific Tagore Garden is organizing the ‘Great Indian Comic Book Festival’, scheduled from April 26...

NCR Saw 29 Land Deals for Nearly 314 Acres Closed in FY-24: ANAROCK Report

New Delhi, April 24, 2024: Delhi-NCR continues to be a hotspot for real estate transactions across various sectors and as in the...

hBits Forays in Pune, Acquires Grade A Commercial Property in Magarpatta

Pune, April 24, 2024: hBits, a leading fractional ownership platform, has marked its entry in Pune with the acquisition of...

-

News3 weeks ago

News3 weeks agoKW Delhi 6 Mall Onboards New Brands

-

News4 weeks ago

Manasum Senior Living Launches IKIGAI GOA, A Senior Living Community in North Goa, in collaboration with Prescon Homes

-

News2 weeks ago

Godrej Properties Sells Rs 3k cr+ Homes of Godrej Zenith, Gurugram, within 3 days

-

News3 weeks ago

Commercial Realty Gets Tech Savvy: Fast Construction, Enhanced Convenience

-

News4 weeks ago

Bridging India Divide: Top 5 Tier- 2 Cities to Focus On

-

News4 weeks ago

Multipoint Connection – A Definite Boon

-

News3 weeks ago

RBI’s Status Quo on Key Policy Rates to Help Maintain the Real Estate Growth Momentum, Say Industry Stalwarts

-

News1 week ago

Olive Announces Dhruv Kalro as Co-Founder