Report

Warehouse leasing is likely to touch 100 mn sq. ft. over the next three years

CBRE South Asia on July 21 announced the findings of its report, tilted ‘India’s Industrial & Warehousing Sector: Tenacious amidst the Turning Tide’. Against the backdrop of robust growth of manufacturing, e-commerce, and third-party logistics (3PL) sectors, the report highlights how Industrial and Warehousing (I&W) activity has gained momentum over the past few years in India.

The report delves into the dynamics of the current manufacturing ecosystem in India and its improving prospects as an alternative supply chain destination on account of elements such as favorable demographics, relatively low labor costs, and continued thrust on infrastructure improvement and policy reforms. As a result, the business climate in the country has vastly improved, as is evident from the continued jump in India’s Ease-of Doing-Business rankings. This, in turn, has had a positive impact on the manufacturing sector of the country, which has attracted over USD 121 billion in FDI inflows over the past six years.

Commenting on the announcement, Anshuman Magazine, Chairman, India & South-East Asia, Middle East & Africa, CBRE, said, “Over the past decade, India has consistently aimed at diversifying from a services-based economy to becoming an alternate manufacturing destination in APAC. As a result, the demand in the Indian I&W sector has surged, making it one of the key growth drivers of the real estate industry. With strong government support to ease investment norms through attractive tax sops and policy initiatives, we can expect increased interest from domestic and global manufacturers.”

Commenting on the announcement, Anshuman Magazine, Chairman, India & South-East Asia, Middle East & Africa, CBRE, said, “Over the past decade, India has consistently aimed at diversifying from a services-based economy to becoming an alternate manufacturing destination in APAC. As a result, the demand in the Indian I&W sector has surged, making it one of the key growth drivers of the real estate industry. With strong government support to ease investment norms through attractive tax sops and policy initiatives, we can expect increased interest from domestic and global manufacturers.”

Even before COVID-19, the manufacturing sector was witnessing a visible shift: away from the previously established destinations towards alternative hubs. As a result, India has increasingly become an active player in the global manufacturing supply chain, on the back of improved domestic capabilities in recent years. This has also been supported by robust Government initiatives such as Make in India, Aatmanirbhar Bharat, Building India Campaign (through the National Infrastructure Pipeline) as well as policies such as the Production Linked Incentive Scheme, aimed at attracting investments across a diverse mix of industries such as electronics, automotive, pharmaceuticals, textiles and food processing among others.

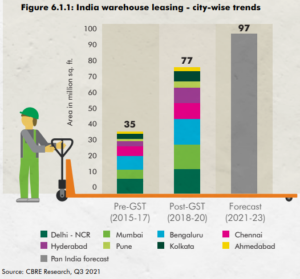

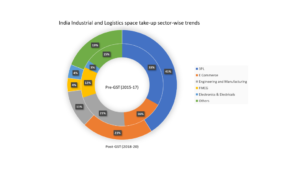

The report also described the current warehouse leasing scenario in the country. The warehousing space take-up over the past five years has crossed 100 million sq. ft. cumulatively, with a historic leasing peak of 32 million sq. ft. reached in 2019. 3PL players accounted for more than 40% of the total warehouse leasing in the post-GST period (2018-20), followed by occupiers from the e-commerce (21%) and engineering and manufacturing (11%) sectors. Occupiers across these sectors have started to increasingly prefer large-sized spaces to consolidate operations, especially post the implementation of the GST. Backed by increasing online retail demand amidst the pandemic, e-commerce and 3PL players are further expected to lead warehouse leasing over the next few years, the report added.

Following a large-scale expansion in tier I cities, occupiers have also started to expand their footprint in tier II and III locations due to improvements in infrastructure and growth of online retail in these areas. Warehouse supply addition over the past five years also crossed 75 million sq. ft. in the country.

In the current scenario, there is a rising demand for an agile supply chain that aims to enable end-to-end control and move from risk mitigation to risk management. As manufacturers focus on increasing CAPEX towards implementing tech in their facility / supply chain, technological advancements such as Artificial Intelligence (AI), Blockchain, Big Data and the Internet of Things (IoT) will ensure that the sector stays resilient in the times to come.

Real Estate, a Huge Employment Generator

The real estate sector in India has been a significant source of employment, with a notable increase observed in recent...

Provident Housing Secures Rs 1,150 Crores Investment from HDFC Capital, with a Potential GDV of Rs 17,100 Crores

Delhi, April 25, 2024: Provident Housing Limited, a wholly owned subsidiary of Puravankara Limited, announced a Rs 1,150 crore investment...

Lohia Global Forays into Real Estate, Earmarks Rs 1000 Crore Investment

New Delhi, April 25, 2024: Lohia Global has announced its venture into the Indian real estate market with Lohia Worldspace. Led by Pyush...

Sumadhura Group Acquires 40 Acres of Residential Land Parcel in Bengaluru

Bengaluru, April 25, 2024: In the midst of a significant upswing in the real estate market in Bengaluru, Sumadhura Group on...

Omaxe Chowk Launches “Filmy” Campaign: Highlights Modern Shopping Experiences in Medieval Chandni Chowk

Delhi, April 24, 2024: Omaxe Chowk, the commercial destination in the heart of Chandni Chowk, Old Delhi, released a ‘film dialogue-based’...

SKA Forays In Luxury Housing: Launches SKA Destiny One in Greater Noida, To Invest Rs 592 Crores

New Delhi, April 24, 2024: NCR based real estate developer, SKA Group announced its foray into the luxury segment and...

-

News4 weeks ago

News4 weeks agoKW Delhi 6 Mall Onboards New Brands

-

News4 weeks ago

Manasum Senior Living Launches IKIGAI GOA, A Senior Living Community in North Goa, in collaboration with Prescon Homes

-

News4 weeks ago

Bridging India Divide: Top 5 Tier- 2 Cities to Focus On

-

News4 weeks ago

Commercial Realty Gets Tech Savvy: Fast Construction, Enhanced Convenience

-

News3 weeks ago

Godrej Properties Sells Rs 3k cr+ Homes of Godrej Zenith, Gurugram, within 3 days

-

News4 weeks ago

Multipoint Connection – A Definite Boon

-

News3 weeks ago

RBI’s Status Quo on Key Policy Rates to Help Maintain the Real Estate Growth Momentum, Say Industry Stalwarts

-

News2 weeks ago

Olive Announces Dhruv Kalro as Co-Founder