News

Data Centre Stock In India To Cross 1,300 MW By 2024 Across Top Seven Cities: CBRE

December 05, 2023: CBRE South Asia Pvt. Ltd, on Tuesday announced the findings of its report ‘From Bytes to Business: India Data Centre Market Powering Progress in 2023’. According to the report, aligning with the country’s progressive digital landscape, India’s Data Centre (DC) capacity is expected to cross ~1,300 MW by the end of 2024 from the current 880 MW (until June 2023). The DC segment growth is likely to continue over 2023-24, with nearly 500 MW currently under construction across several cities. Mumbai, Chennai, and Bangalore will collectively dominate DC stock with an 80% share by the end of 2024. The Indian DC industry is witnessing a continuous uptrend owing to rapid digitalisation, enhanced tech infrastructure and the inclusion of advanced technologies such as 5G, Artificia Intelligence (AI), blockchain and cloud computing.

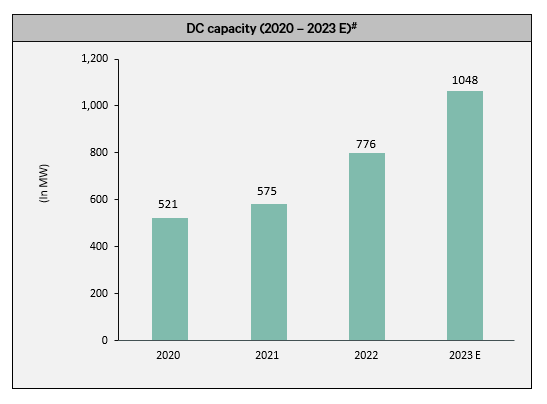

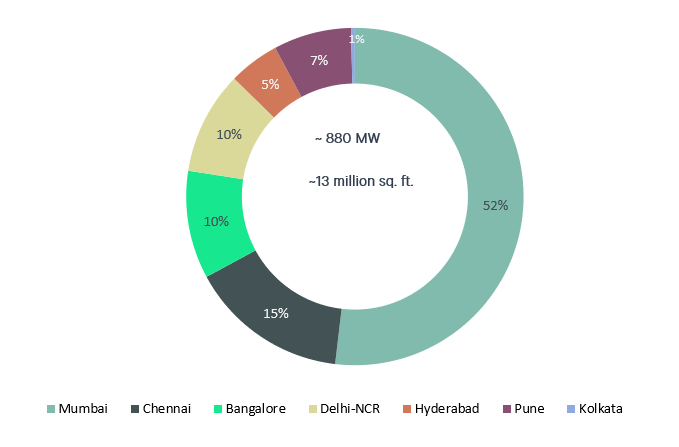

As per the report, India’s DC capacity has doubled over the last four-five years to reach ~ 880 MW as of June 2023 and is expected to increase further to touch ~1,048 MW by the end of 2023. During Jan-Jun 2023, the DC stock in the top 7 cities in India stood at ~880 MW capacity spanning over 13 million sq. ft. Mumbai, Chennai, Bangalore, and Delhi-NCR accounted for about 87% of the country’s DC stock as of June 2023. Overall, DC occupancy levels in India stood at about 75 – 80% in Jan-Jun’23, which is likely to improve further by the end of the year.

Snapshot of the DC stock in India (as of H1 2023)

Mumbai continues to be the most prominent DC market in the country, accounting for more than half of the total stock (52%) as of Jun’23. The city is expected to lead the supply addition with a 46% share of the upcoming 500 MW by the end of 2024. The presence of multiple cable landing stations, inclusive government initiatives, and well-rooted entertainment and finance industries have established the city as a top destination for BFSI, media, cloud, and OTT companies to locate their DC operations.

Chennai has also emerged as a key established tier 1-DC market in India, accounting for 21% of the total stock in the top 7 cities as of Jun’23. The city is expected to account for a 21% share of the upcoming 500 MW supply by the end of 2024. Until Jun’23, Bangalore and Delhi-NCR accounted for 10% of DC stock each.

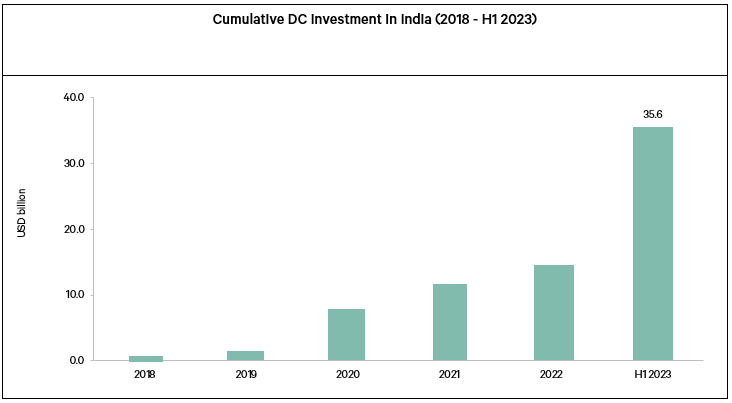

Further, the country’s growing digital infrastructure, increasing technology penetration, and proactive regulatory push have made it an attractive destination for DC investments. During the 2018 – June’23 period, the DC market in India attracted investment commitments of about USD 35 billion by both global and domestic investors, the report highlighted. Hyperscale DCs dominated most of the DC investments with a share of about 89%, while colocation DCs contributed to the rest of 11%. The top states that dominated the cumulative investment commitments include Maharashtra, Tamil Nadu, West Bengal, and Uttar Pradesh.

Anshuman Magazine, Chairman & CEO – India, South-East Asia, Middle East & Africa, CBRE, said, “Increasing population, enhanced use of technology, social media, and online streaming platforms, rising need for data localisation and fast improving digital infrastructure would continue to boost demand for data centres in India. This, in turn, is likely to result in the country becoming one of the largest DC destinations across APAC over the next decade. We also anticipate heightened interest from investors looking to capitalize on DC’s attractiveness as a preferred alternate real estate option in the country. Multiple state governments in India have been giving an enormous push to the DC segment in the country, with dedicated policies/incentives introduced to attract both global and domestic investors. Most of the states have also declared DCs under ‘essential services’ to ensure uninterrupted operations throughout the year.”

Ram Chandnani, Managing Director, Advisory & Transactions Services, CBRE India, said, “ Investor interest in the Indian DC market remains elevated despite the recent economic headwinds. Technology companies, along with corporates from sectors such as BFSI, Cloud Services and OTT platforms will continue to drive DC demand in India. Further, public sector undertakings and other key government enterprises are shifting to third-party colocation DCs due to an increased focus on digitization and e-governance to ease operations. Though the DC industry is witnessing an expansion in tier-I cities, leading hyperscalers and cloud service providers are also likely to expand to tier-II cities to capture the growing demand among BFSI firms and online streaming platforms to establish DC facilities closer to the consumption hubs.”

Outlook for Data Centres

- Technology firms, BFSI companies, cloud services and OTT platforms would continue to be key demand drivers for both colocation and hyperscale DC facilities

- Several engineering & manufacturing firms and technology companies are also likely to set up DCs for R&D labs

- The exponential growth in AI-generated data workload is expected to drive demand for high power density DC facilities (~ more than 30kW / rack) as compared to traditional power density facilities (~ 8-10kW / rack)

- PSUs and other government enterprises would continue to focus on the deployment of operations to third-party colocation DCs

- Small- to medium-sized corporates would continue to gradually shift operations from enterprise to colocation DCs

- DC operators are also likely to expand in tier-II DC markets to capture the growing demand among BFSI firms and online steaming platforms to establish DC facilities closer to the consumption hubs

- Operators should provide tailor-made streamlined DC solutions along with scalability options to attract occupiers looking for flexibility / agility in the future

- Increased focus on sustainability measures and minimising energy usage would achieve cost efficiencies

- DC investors should continuously explore opportunities to upgrade facilities to increase efficiencies, reduce costs and support the environment through smart investments, IT strategies and energy management

- ESG, machine learning and AI are likely to take centre stage in DC investments

- In addition to power and infrastructure availability, regulatory hurdles in terms of land acquisition and delay in approvals are expected be a key challenge for investors in select cities

- Build-to-suit, acquisition and equity investments remain the preferred investment routes into the sector in India. Investors are also likely to form partnerships with experienced operators and developers to gain exposure to the sector. This approach enables investors to leverage their partner’s expertise in areas such as site selection, operations, and regulatory compliance

Godrej & Boyce and Godrej Properties to continue their association for land development in Vikhroli

Dateline: Mumbai: Godrej & Boyce, the owner-developer, and Godrej Properties, the development manager, announced that the two companies will continue...

Godrej Family Announces Realignment Of Their Shareholding In Godrej Companies

Mumbai, April 30, 2024: The Godrej family on Tuesday announced an ownership realignment of their shareholdings in the Godrej Companies. The...

Luxury Housing Grows 10% Y-o-Y in Jan-Mar, 2024 Across Top Seven Cities: CBRE

April 30, 2024: CBRE South Asia Pvt. Ltd., announced the findings of its report, ‘India Market Monitor Q1 2024’. According...

Azim Syed is CFO & CRIO, RHI Magnesita

Gurugram, April 30, 2024: RHI Magnesita India Ltd, leading manufacturer and supplier of high-grade refractory products, systems and solutions –...

SEBI supports regularization of Fractional Ownership Platforms: Market float of up to Rs 4.5k bn available through complete listing of strata office assets by 2026

Gurugram, April 30, 2024: With Securities and Exchange Board of India (SEBI) formulating detailed guidelines for Small and Medium REITs...

White Lotus Group Appoints Chetan CI, IIM Alumnus, as Chief Operating Officer

Bengaluru, April 29, 2024: White Lotus, announced the appointment of Chetan CI as its new Chief Operating Officer. Chetan is...

-

News3 weeks ago

News3 weeks agoGodrej Properties Sells Rs 3k cr+ Homes of Godrej Zenith, Gurugram, within 3 days

-

News4 weeks ago

RBI’s Status Quo on Key Policy Rates to Help Maintain the Real Estate Growth Momentum, Say Industry Stalwarts

-

News2 weeks ago

Noida’s High-Rise Societies Face Multiple Challenges Despite Rapid Urban Growth

-

News2 weeks ago

Olive Announces Dhruv Kalro as Co-Founder

-

News3 weeks ago

Godrej Properties Sells 5000+ Homes of Rs 9.5 cr in Q4FY24, Bookings up 84% YoY

-

News3 weeks ago

Vestian: Domestic Investors Dominate Institutional Investments in Jan-Mar’24

-

News2 weeks ago

News2 weeks agoIndia to become the fastest-growing silver economy, housing up to 17% of the world’s elderly population by 2050: CBRE Report

-

News3 weeks ago

HRERA Gurugram Rejects Godrej Properties’ Project Extension Application, Account Frozen For Prolonged Non-compliances