News

Demand For Commercial Space Hits A New Peak Of 69.4 Msf, Rising By A Significant 40% Y-o-Y: Cushman & Wakefield India

National, 13th January 2020: Gross office leasing volumes pan-India touched a phenomenal high of 69.4 msf in 2019, compared to 49.5 msf in 2018. Market demand for commercial office spaces stayed strong throughout the year. Record breaking pre-leasing activity was recorded, vacancy stayed low despite robust supply, rentals increased, and co-working space take-up rose 1.43X compared to 2018, as per the market analysis by Cushman & Wakefield India. We highlight key aspects that made 2019 a strong year for commercial leasing.

National, 13th January 2020: Gross office leasing volumes pan-India touched a phenomenal high of 69.4 msf in 2019, compared to 49.5 msf in 2018. Market demand for commercial office spaces stayed strong throughout the year. Record breaking pre-leasing activity was recorded, vacancy stayed low despite robust supply, rentals increased, and co-working space take-up rose 1.43X compared to 2018, as per the market analysis by Cushman & Wakefield India. We highlight key aspects that made 2019 a strong year for commercial leasing.

2019 WAS THE YEAR FOR FLEXIBLE WORKSPACES:

| Sector | 2018 | 2019 |

| IT/BPM | 33.3% | 32.6% |

| Captive Centers | 26.8% | 19.8% |

| Flexible Workspaces | 9.9% | 10.1% |

| *Cushman & Wakefield Research India | ||

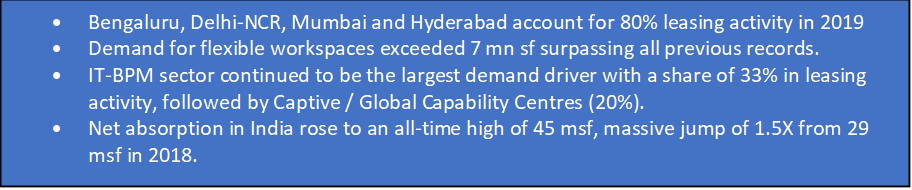

Flexible workspaces have leased more than 7 msf in 2019, a new record in the Indian commercial leasing landscape. India Inc has acknowledged the merits these spaces offer and are now a strategic imperative for occupiers as part of their real estate portfolio planning. Corporates have leased more than 100,000 seats with large operators in the country over the last two years. Delhi-NCR has the largest share of flexible working space demand at 2.4 msf (a 94% rise y-o-y) followed by Bengaluru, 1.7 msf. Flex-space demand in Pune has touched 1.0 msf this year, a 3-fold rise on an annual basis.

IT-BPM sector continued to be the largest demand driver in 2019 with a share of 32.6% in leasing activity followed by Captive / Global Capability Centres (19.8%).

CITY WISE OFFICE LEASING STATISTICS:

Gross leasing volumes: Bengaluru topped the charts at 16.47 msf of demand followed by Delhi-NCR (13.95 msf), Mumbai (13.9 msf) and Hyderabad (10.7 msf).

| Gross Leasing Volume (in msf) | 2018 | 2019 | Growth (in percent) |

| Mumbai | 4.49 | 13.95 | 211% |

| Delhi NCR | 11.14 | 13.95 | 25% |

| Bengaluru | 14.45 | 16.47 | 14% |

| Chennai | 2.48 | 5.85 | 136% |

| Pune | 6.09 | 4.96 | -19% |

| Hyderabad | 10.00 | 10.74 | 7% |

| Kolkata | 0.61 | 1.83 | 201% |

| Ahmedabad | 0.32 | 1.52 | 368% |

| PAN India | 49.57 | 69.27 | 40% |

Net absorption: Net absorption in India rose to an all-time high of around 45 msf, a massive increase of 1.56X from 29 msf in 2018.

| Net Absorption (in msf) | 2018 | 2019 | Growth (in percent) |

| Mumbai | 3.2 | 5.18 | 62.9% |

| Delhi NCR | 4.8 | 9.85 | 106.1% |

| Bengaluru | 7.5 | 9.26 | 23.5% |

| Chennai | 2.4 | 1.79 | -25.1% |

| Pune | 3.9 | 5.06 | 28.8% |

| Hyderabad | 6.0 | 10.01 | 66.5% |

| Kolkata | 0.4 | 1.41 | 219.5% |

| Ahmedabad | 0.6 | 2.24 | 284.2% |

| PAN India | 28.8 | 44.8 | 55.5% |

Vacancy rates: At 3.6%, office vacancy in Pune has dropped to the lowest in the country followed by Bengaluru (5.2%), Hyderabad (5.5%) and Chennai (9.7%).

| Vacancy Rate (%) | 2018 | 2019 |

| Mumbai | 19.9% | 18.8% |

| Delhi NCR | 23.6% | 23.4% |

| Bengaluru | 5.8% | 5.2% |

| Chennai | 9.6% | 9.7% |

| Pune | 6.8% | 3.6% |

| Hyderabad | 6.4% | 5.5% |

| Kolkata | 38.1% | 35.7% |

| Ahmedabad | 36.5% | 43.9% |

| PAN India | 14.7% | 14.3% |

Supply: New supply rose 47% y-o-y to 50.6 msf during the year, with Delhi-NCR accounting for the largest share at 27%, where new completions have grown by a massive 140% during the year. Meanwhile, office stock in Hyderabad has grown by 21% y-o-y with new supply of 10 msf during the year.

| New Completions (in msf) | 2018 | 2019 | Growth (in percent) |

| Mumbai | 5.6 | 5.2 | -6.8% |

| Delhi NCR | 5.6 | 13.4 | 140.5% |

| Bengaluru | 9.2 | 8.8 | -4.2% |

| Chennai | 2.8 | 2.0 | -27.6% |

| Pune | 3.1 | 3.9 | 25.7% |

| Hyderabad | 5.5 | 10.1 | 84.4% |

| Kolkata | 0.6 | 1.3 | 105.0% |

| Ahmedabad | 1.9 | 5.8 | 198.5% |

| PAN India | 34.4 | 50.6 | 47.2% |

Pre-commitment activity: 2019 also saw a record high preleasing activity at 17.2 msf, a 7.2% y-o-y growth. Hyderabad saw pre-commitments of 5.8 msf, garnering 34% share of the total followed by Bengaluru ay 4.7 msf (27%). Healthy pre-leasing demand was also witnessed in Delhi-NCR, Mumbai and Chennai.

| Pre-commitments (in msf) | |||

| City | 2018 | 2019 | Growth (in percent) |

| Mumbai | 0.08 | 2.00 | 2258.5% |

| Delhi NCR | 1.86 | 2.19 | 17.8% |

| Bengaluru | 5.54 | 4.69 | -15.4% |

| Chennai | 0.21 | 1.34 | 543.1% |

| Pune | 3.12 | 1.20 | -61.4% |

| Hyderabad | 5.26 | 5.80 | 10.4% |

| Kolkata | 0 | 0 | N/A |

| Ahmedabad | 0 | 0 | N/A |

| PAN India | 16.07 | 17.22 | 7.2% |

| “Commercial leasing volumes touched 69.4 msf in 2019, a phenomenal increase of 40% compared to 2018. Flexible workspaces hit a high note with 7 msf share in gross leasing. Interestingly this figure exceeds 2018 and 2017 combined. Occupiers from the IT space expanded their RE portfolio aggressively and contributed to the maximum share of leasing activity across sectors. Among major metros, Hyderabad & Delhi-NCR noted unprecedented net absorption activity, Mumbai markets saw pre-commitment activity increase over twenty-fold compared to 2018, and Bengaluru led the market in gross leasing. On many notes, the office leasing performance in India surpassed industry expectations and paves the way for an optimistic year ahead.” Anshul Jain, Country Head & Managing Director, Cushman & Wakefield India |

Provident Housing Secures Rs 1,150 Crores Investment from HDFC Capital, with a Potential GDV of Rs 17,100 Crores

Delhi, April 25, 2024: Provident Housing Limited, a wholly owned subsidiary of Puravankara Limited, announced a Rs 1,150 crore investment...

Lohia Global Forays into Real Estate, Earmarks Rs 1000 Crore Investment

New Delhi, April 25, 2024: Lohia Global has announced its venture into the Indian real estate market with Lohia Worldspace. Led by Pyush...

Sumadhura Group Acquires 40 Acres of Residential Land Parcel in Bengaluru

Bengaluru, April 25, 2024: In the midst of a significant upswing in the real estate market in Bengaluru, Sumadhura Group on...

Omaxe Chowk Launches “Filmy” Campaign: Highlights Modern Shopping Experiences in Medieval Chandni Chowk

Delhi, April 24, 2024: Omaxe Chowk, the commercial destination in the heart of Chandni Chowk, Old Delhi, released a ‘film dialogue-based’...

SKA Forays In Luxury Housing: Launches SKA Destiny One in Greater Noida, To Invest Rs 592 Crores

New Delhi, April 24, 2024: NCR based real estate developer, SKA Group announced its foray into the luxury segment and...

Unlocking Investment Potential: Exploring Yamunanagar’s Real Estate Landscape

By: Ravi Saund, Founding Director, Emperium Nestled in the heart of Haryana, Yamunanagar is not just any ordinary city; it’s...

-

News4 weeks ago

News4 weeks agoKW Delhi 6 Mall Onboards New Brands

-

News4 weeks ago

Manasum Senior Living Launches IKIGAI GOA, A Senior Living Community in North Goa, in collaboration with Prescon Homes

-

News4 weeks ago

Bridging India Divide: Top 5 Tier- 2 Cities to Focus On

-

News4 weeks ago

Commercial Realty Gets Tech Savvy: Fast Construction, Enhanced Convenience

-

News3 weeks ago

Godrej Properties Sells Rs 3k cr+ Homes of Godrej Zenith, Gurugram, within 3 days

-

News4 weeks ago

Multipoint Connection – A Definite Boon

-

News3 weeks ago

RBI’s Status Quo on Key Policy Rates to Help Maintain the Real Estate Growth Momentum, Say Industry Stalwarts

-

News1 week ago

Olive Announces Dhruv Kalro as Co-Founder