News

FY25 Residential Demand, Price Growth to Moderate, Segment Bi-polarisation to Undergo Course Correction: Ind-Ra Report

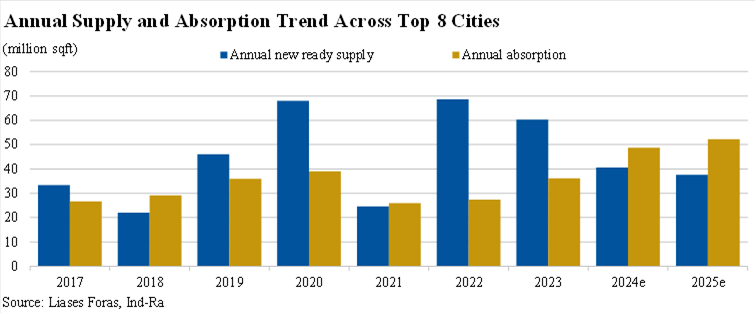

Mumbai. April 23, 2024: India Ratings and Research (Ind-Ra) has maintained a neutral outlook for the residential real estate sector for FY25. Absorption and prices are likely to be supported by affordability and stability of interest rates. However, given the high base of FY24, the growth rates are likely to taper down. The residential real estate market registered a strong performance in 9MFY24 where the sales growth exceeded 25% yoy for the top eight real estate clusters, despite price increases and sticky interest-rates.

“With most regions witnessing a surge in prices, Ind-Ra expects the pre-sales growth to moderate to 8% to 10% yoy in FY25. Inventory levels have also risen over FY24 in the premium and luxury segment, as launches increased encouraged by the sharp rise in sales and realisations,” says Mahaveer Shankarlal Jain, Director, Corporate Ratings, Ind-Ra.

Housing Price Rise Appears Sustainable: Ind-Ra expects the prices to have been higher 22% yoy at end-FY24 and would be subdued at around 5% yoy for FY25, due to the base-effect and large amount of new launches planned. With most of the old-stock cleared and existing inventory largely liquidated along with a continued pick-up in demand and spike in commodity prices due to geopolitical tensions, prices surged by almost 14% yoy in FY23 along with an increase in land prices and rental yields.

Demand Shifting towards Mid- & Upper-mid Income Segments from Luxury and Premium Segments: Ind-Ra expects the mid-income and upper mid-income segments, which emerged as the leading consumer segments in 9MFY24 (30% and 28% of the overall home sales respectively), to continue to witness a strong buyer interest. While the premium and luxury segments witnessed sharp demand growth in 9MFY24, Ind-Ra expects them to cool down due to the high base as the unsold inventory levels remain elevated and are the highest over the past five years.

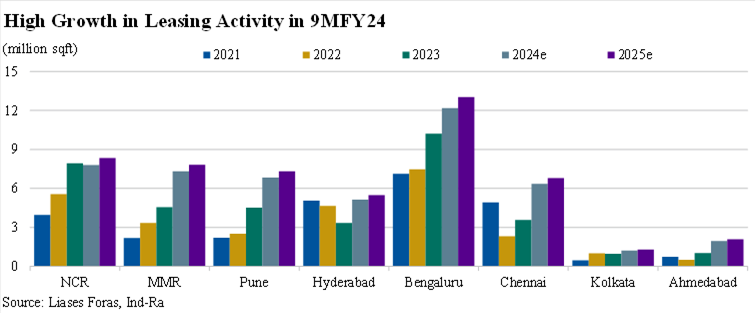

Tier II and III Cities to Report Significant Growth: Renewed government focus on developing infrastructure and improving connectivity across new cities, with mega projects such as highways, airports, metros, and digitisation, is likely to stimulate the development of Tier II and III cities and generate substantial growth. While the relatively new markets of Thiruvananthapuram, Guwahati, Rajkot and Ranchi market are witnessing exponential growth in housing, Outer MMR, Surat, Vadodara, Jaipur, Nashik, Chandigarh and Bhopal forming over 60% of the market in terms of the units sold, grew at a CAGR by 14% during 2021-2023.

Affordability Levels Marginally Dip in FY24, Likely to Sustain in FY25: A series of repo rate hikes of 250bp over FY23 had a sharp impact on affordability, challenging the demand dynamics in the affordable segment as it led to lower disposable incomes among the target customers. Coupled with higher mortgage rates, reduced loan eligibility, and an increase in down payments, this resulted in a steep decline in demand for the affordable segment. With prices expected to further increase over FY25, albeit moderately, affordability levels are likely to remain challenging, leading to deferment in purchases. Developers have also responded to the situation by reducing the supply of affordable inventory.

Bipolarisation Could Moderate with Improvement in Non-Tier I Players’ Performance: Tier I players had been gaining market share through FY21 to FY23, as homebuyers across the top tier cities continued to prefer established and reputed players. However, as the affordability dipped and buyers looked for alternatives to premium priced apartments and houses by Tier I players, the performance of other players improved. While Ind-Ra expects Tier I residential players to continue to lead and generate strong sales, considering the market consolidation in their favour and goodwill & brand recognition among customers, such consolidation is expected to moderate.

Lavish Lifestyle & High Returns: Invest in Sector 71 at SPR in Gurugram

By: Ashwani Kumar, Pyramid Infratech Adjacent to Gurugram’s fast-emerging residential hubs Southern Peripheral Road and Golf Course Extension Road, Sector...

Max Estates Announces Strategic Joint Development Agreement in Gurugram

May 3, 2024: Max Estates Limited (Max Estates), the real estate arm of the Max Group, on Friday announced execution of...

FY25 Construction Outlook: Steady Performance in Election Year; All Eyes on Private Capex: Ind-RA

Ind-Ra-Hyderabad-3 May 2025: India Ratings and Research (Ind-Ra) has maintained a neutral outlook on the construction sector for FY25, while...

Sunteck Realty, Westside Collaborate to Showcase Luxury & Style

Mumbai, May 3, 2024: Sunteck Realty and Westside have collaborated to embark on a long term association to embellish the show residences of...

Birla Estates Launches Silas at Birla Niyaarain Mumbai, Clocks Over Rs 2.5kCr Sales

DELHI, May 3, 2024: Birla Estates Pvt. Ltd., announced record sales of its signature tower Silas at Birla Niyaara clocking...

Construction Quality is the Key to Winning the Trust of the Customers

May 3, 2024: With the Indian real estate at the cusp of a major boom, it has brought limelight on...

-

News4 weeks ago

News4 weeks agoGodrej Properties Sells Rs 3k cr+ Homes of Godrej Zenith, Gurugram, within 3 days

-

News4 weeks ago

RBI’s Status Quo on Key Policy Rates to Help Maintain the Real Estate Growth Momentum, Say Industry Stalwarts

-

News2 weeks ago

Noida’s High-Rise Societies Face Multiple Challenges Despite Rapid Urban Growth

-

News3 weeks ago

Olive Announces Dhruv Kalro as Co-Founder

-

News4 weeks ago

Godrej Properties Sells 5000+ Homes of Rs 9.5 cr in Q4FY24, Bookings up 84% YoY

-

News3 weeks ago

Vestian: Domestic Investors Dominate Institutional Investments in Jan-Mar’24

-

News2 weeks ago

News2 weeks agoIndia to become the fastest-growing silver economy, housing up to 17% of the world’s elderly population by 2050: CBRE Report

-

News3 weeks ago

HRERA Gurugram Rejects Godrej Properties’ Project Extension Application, Account Frozen For Prolonged Non-compliances