News

Global Capability Centres to Lease 60-62 mn sq ft Office Space in 2023-25 Across Top 6 Cities: CBRE

November 16, 2023 – CBRE South Asia Pvt. Ltd, on Thursday announced the findings of its report ‘India’s Global Capability Centres-charting a new technology era’. The report elaborates on the growth of Global Capability Centres (GCCs) in India, leasing preferences, and key drivers for expansion.

As per the report, GCCs are likely to lease office space of around 60-62 mn. sq. ft. of space between 2023-25. Sectors including technology, BFSI and engineering & manufacturing will lead leasing activity, while sectors such as life sciences, automobiles, and aviation will also expand their GCC operations in India. Cementing the long-term intent of global corporates in India, GCCs are now leasing larger offices with the potential to scale up in the future. North American firms continue to be the mainstay of GCCs in India. Availability and cost of talent, real estate, and supporting regulatory framework aid GCCs expansion in India.

By 2025, it is estimated that there will be ~1900 total operational GCCs in the country from existing ~1580. During this period, GCC leasing activity is expected to account for 35-40% of the overall office leasing. Globally, among the top emerging GCC hubs, including Brazil, Chile, China, Czech Republic, Hungary, Philippines, and Poland, India has the best cost and talent attractiveness score, which makes the country the most sought-after destination for GCCs.

City Top micro markets inupcoming supply (2023-2025F) Delhi-NCR Noida Expressway;Extended Golf Course Road Mumbai Navi Mumbai;Extended Business District Bangalore North Bangalore ;Outer Ring Road Chennai OMR Zone 2;Mount Poonamallee Road Hyderabad IT Corridor 2;Extended IT Corridor Pune PBD North-East;SBD North-West

The report also states that from 2023-25, the top six cities, including Delhi, Bangalore, Mumbai, Chennai, Pune and Hyderabad, are likely to witness a strong pipeline of new developments in emerging micro markets, creating new hubs for activity. The upcoming developments would be geared towards quality investment-grade office supply, giving GCCs ample scope to upgrade and scale as they expand.

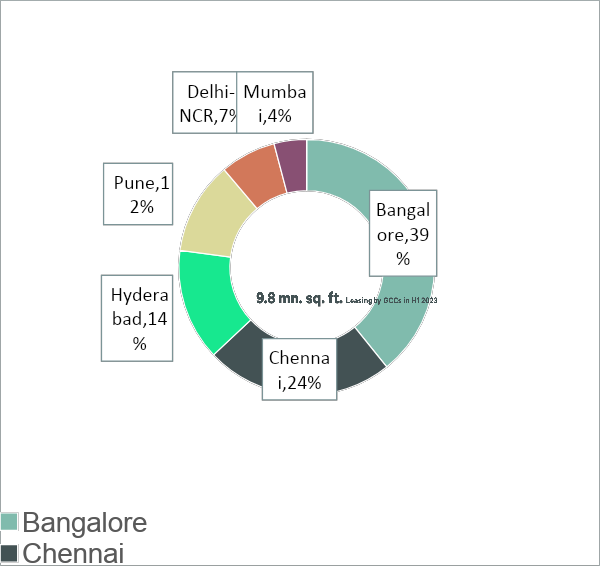

During Jan-Jun’23, GCCs continued aggressive expansion and accounted for a 38% share in overall office space take-up across 6 cities. Office leasing by GCCs in Jan-Jun’23 stood at 9.8 mn. sq. ft.

Bangalore, Chennai, and Hyderabad – cumulatively accounted for over 77% of the total GCC leasing during Jan-Jun’23. Bangalore continues to account for the largest share in leasing over the six months (Jan’23-Jun’23), while Chennai has witnessed about one-fourth share led by ready institutional supply that entered the market in 2023.

For Bangalore, GCC leasing during Jan-Jun’23 stood at 3.8 mn. sq. ft. Between Jan- Dec’22 and Jan-Jun’23, key micro markets for GCC leasing were Outer Ring Road and Whitefield. In Bangalore, GCC leasing quantum between Jan- Dec’22 and Jan-Jun’23 stood at 13 mn sq. ft., propelled by the tech sector that accounted for 46% share. Over the past few years, the GCC landscape in the city has evolved from being overtly dominated by technology and BFSI firms, to now becoming more diversified (as well as niche and specialised) with firms from sectors such as retail, aerospace and life sciences expanding their footprint in the city.

During Jan-Jun’23, Chennai emerged as the second preferred GCC market after Bangalore in India with, 2.4 mn. sq. ft. space take- up. Between Jan- Dec’22 and Jan-Jun’23, key micro markets for GCC leasing in Chennai were OMR Zone I and PT Road. GCC leasing quantum in the city, between Jan-Dec’22 and Jan-Jun’23 stood at 4 mn sq. ft. with a 39% share dominated by the E&M sector. The city has witnessed about a two-fold increase in GCC leasing in the Jan-Jun’23 period as compared to Jan-Jun’22.

City % of GCCs leasing share in office sector (2022- H1 2023) Office space leasing (mn. sq. ft.) Bangalore 44% 13 Hyderabad 20% 6 Chennai 13% 4 Pune 10% 3

Chennai is also an education hub, with a high presence of colleges and universities offering science, technology, engineering, and mathematics (STEM) courses, a key driver for attracting new GCC entrants into the city. The Tamil Nadu R&D Policy 2022, wherein entities such as GCCs and R&D centres are eligible for a range of incentives on electricity and stamp duty costs, is likely to auger well for global firms looking to set up their footprint in the city.

Hyderabad remains in the top three cities driving space absorption by GCCs during Jan-Jun’23. Leasing by GCCs during Jan-Jun’23 in the city stood at 1.4 mn. sq. ft. Between Jan- Dec’22 and Jan-Jun’23, key micro markets for GCC leasing were IT Corridor II and Extended IT Corridor. GCC leasing quantum between Jan-Dec’22 and Jan-Jun’23 is 6 mn sq. ft. with a 35% share dominated by the tech sector companies. The growth of GCCs in the city comes in the backdrop of ample talent availability and an improving standard of living, comparatively lower costs, amidst proactive government initiatives. The city has witnessed GCC activity from across sectors such as technology, life sciences and consulting services.

Furthermore, Pune is emerging as a GCC hub, with a 57% increase in space take up in Jan-Jun’23 compared to Jan-Jun’22. GCC leasing quantum between Jan-Dec’22 and Jan-Jun’23 stood at 3 mn sq. ft. with 42% share dominated by the technology sector.

Anshuman Magazine, Chairman & CEO – India, South-East Asia, Middle East & Africa, CBRE, said, “India has emerged as the most preferred destination for GCCs worldwide, and the growth of GCCs in India is a testament to the country’s skilled talent, cost efficiency, favourable business environment, and government support. Post the pandemic, global firms were nudged to re-evaluate their business offerings to increase digitisation levels. In a bid to ensure business agility, improve efficiency and make their businesses resilient, a higher number of MNCs explored multi-functional GCCs in India. Gradually, mid, and smaller-sized firms also started venturing into the Indian shores to enhance their offerings.

Companies are also evaluating tier-II cities to set up their GCCs and expand their operations, encouraged by availability of talent due to the reverse migration observed during the pandemic, led by remote and hybrid working models. While cost arbitrage in tier-II cities has always been an advantage towards emerging hubs, the recent thrust on infrastructure development in these cities has also added to advantage of non-metro cities. Going forward, the country’s maturing startup industry, which has a symbiotic relationship with the GCC sector, is likely to see greater collaborations, fuelling the growth of the global centres’ innovation ecosystem”.

Ram Chandnani, Managing Director, Advisory & Transactions Services, CBRE India, said, “From a commercial real estate perspective, GCCs in India form a large occupier group and are often the first to adapt and innovate, setting a precedence for other occupier groups. Most GCCs in India continue to adopt a hybrid workstyle, they will likely continue to take up large office space to enhance collaboration and innovation – key performance enablers for most GCCs. We believe that the incremental growth over the next two-three years will continue to be across the top metro cities. From a workplace perspective, the health and well-being of employees will continue to be of paramount significance for GCCs, with offices built for a multi-generational workforce”.

Building a Sustainable Chennai: IGBC’s E3 Event Drives Green Building Practices

Chennai, April 27, 2024: Indian Green Building Council (IGBC) organised an event towards sustainable development in Chennai and beyond. In...

Jus’Jumpin’ Opens at Urban Square Mall

Udaipur, April 27, 2024: Urban Square Mall, Udaipur’s largest shopping and entertainment destination, announced its exciting partnership with Jus’ Jumpin’....

Delhi-NCR’s Luxury Real Estate Soars: Q1 2024 Report Unveils High-End Housing Boom

April 27, 2024: Luxury real estate sector continues to raise the bar in Q1 2024. A recent report by Cushman...

Real Estate, a Huge Employment Generator

The real estate sector in India has been a significant source of employment, with a notable increase observed in recent...

Provident Housing Secures Rs 1,150 Crores Investment from HDFC Capital, with a Potential GDV of Rs 17,100 Crores

Delhi, April 25, 2024: Provident Housing Limited, a wholly owned subsidiary of Puravankara Limited, announced a Rs 1,150 crore investment...

Lohia Global Forays into Real Estate, Earmarks Rs 1000 Crore Investment

New Delhi, April 25, 2024: Lohia Global has announced its venture into the Indian real estate market with Lohia Worldspace. Led by Pyush...

-

News4 weeks ago

News4 weeks agoKW Delhi 6 Mall Onboards New Brands

-

News3 weeks ago

Godrej Properties Sells Rs 3k cr+ Homes of Godrej Zenith, Gurugram, within 3 days

-

News4 weeks ago

Commercial Realty Gets Tech Savvy: Fast Construction, Enhanced Convenience

-

News3 weeks ago

RBI’s Status Quo on Key Policy Rates to Help Maintain the Real Estate Growth Momentum, Say Industry Stalwarts

-

News2 weeks ago

Olive Announces Dhruv Kalro as Co-Founder

-

News1 week ago

Noida’s High-Rise Societies Face Multiple Challenges Despite Rapid Urban Growth

-

News3 weeks ago

Godrej Properties Sells 5000+ Homes of Rs 9.5 cr in Q4FY24, Bookings up 84% YoY

-

News2 weeks ago

Vestian: Domestic Investors Dominate Institutional Investments in Jan-Mar’24